Facility Managers and Financial Controllers in the GCC share two universal goals: lowering operational costs and mitigating risk. Usually, these goals are tackled separately, engineers look at utility bills, while risk managers look at insurance policies. However, there is a critical engineering metric that bridges this gap: Power Factor (PF).

Most businesses view Power Factor Correction (PFC) solely as a way to avoid utility penalty charges. But could an engineering study, typically performed for energy efficiency, also be a powerful tool for negotiating better insurance terms? The answer lies in the direct link between electrical efficiency and physical safety. By commissioning a professional power system analysis and design strategy, you are not just optimizing energy; you are demonstrating a proactive approach to electrical risk management that savvy insurers value highly.

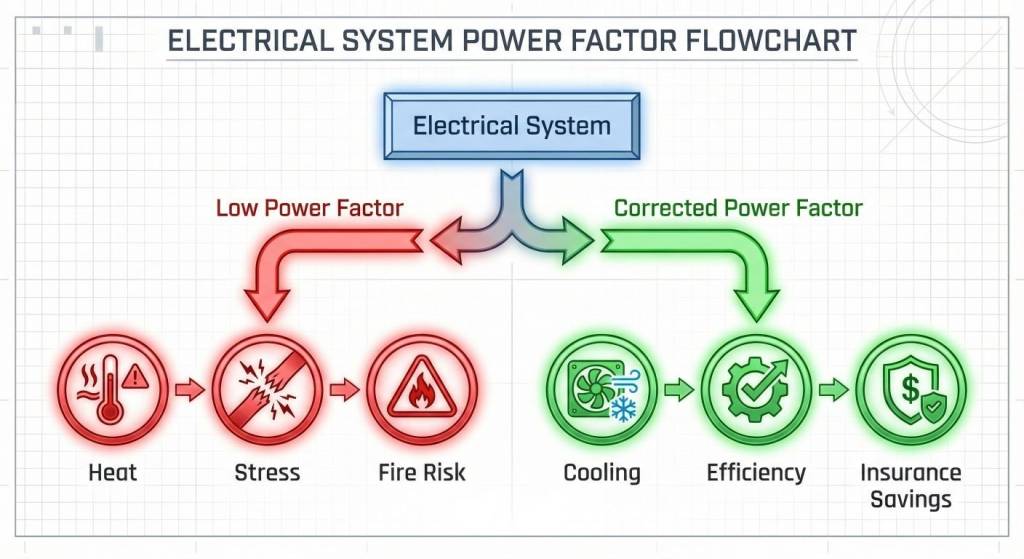

The Technical Link: How Poor Power Factor Increases Physical Risk

To understand why an insurer cares about your Power Factor, we must look at the physics. Low Power Factor means your system is drawing more current than is necessary to do useful work. This “reactive current” circulates through your cables, transformers, and switchgear, serving no purpose other than generating excess heat.

This chronic thermal stress is a silent enemy. It accelerates the aging of insulation, causes connections to loosen over time, and significantly increases the probability of equipment failure, arc flash, or electrical fire. By addressing this through a technical analysis power system health check, you are directly targeting the root cause of many industrial fires.

Need to assess your system’s health? Explore our Power Systems Analysis and Insurance & Risk Management services.

The Insurance Perspective: How Underwriters View Electrical Risk

Insurance underwriting is evolving. Insurers are increasingly using data and engineering insights to model risk rather than relying solely on historical claims. A facility with a history of electrical incidents, or one that cannot demonstrate a rigorous preventive maintenance strategy, is viewed as a high-risk asset.

A professional power quality study for insurance purposes serves as tangible evidence of proactive risk management. When you present a completed study and evidence of the corrective actions taken, you change the narrative. You prove to the underwriter that you understand your internal hazards and are actively mitigating them. This moves your facility from a “high risk” category to a “managed risk” category in the eyes of the insurer.

The Two-Pronged Financial Benefit: Direct vs. Indirect Savings

Investing in a specialized power systems analysis and design study delivers a Return on Investment (ROI) on two fronts.

1. Direct Utility Savings (The Immediate ROI)

This is the most visible benefit. In many GCC jurisdictions, utilities impose heavy penalty charges for low PF (typically below 0.9 or 0.95). These penalties can amount to 5-20% of your total electricity bill. Eliminating these charges often pays for the study and the installation of capacitor banks within 12-24 months.

2. Indirect Risk-Based Savings (The Strategic Value)

While utility savings pay for the equipment, the risk benefits pay for the peace of mind.

- Potential Premium Reduction: While not guaranteed, an improved risk profile is a strong lever in negotiation.

- Avoided Premium Increases: Demonstrating risk control is your best defense against market-wide rate hikes at renewal.

- Business Interruption (BI) Value: The core benefit is business interruption risk mitigation. Preventing a fire or a main transformer failure protects your deductible and ensures your insurability remains intact.

The Step-by-Step Process: From Study to Savings

How do you turn this engineering concept into a financial win? Follow this roadmap.

Step 1: Commission a Detailed Power Factor & Harmonic Study

This is not a simple meter reading. It involves logging data over weeks to capture load variations and identifying harmonic distortions. Harmonics are critical; installing capacitors without analyzing harmonics can cause resonance, which damages equipment.

Step 2: Implement the Recommended Solution

Based on the study, install correctly sized and located capacitor banks or active harmonic filters. Professional design is essential to ensure the equipment integrates safely with your existing infrastructure.

Step 3: Document the Improvement and Engage Your Insurer

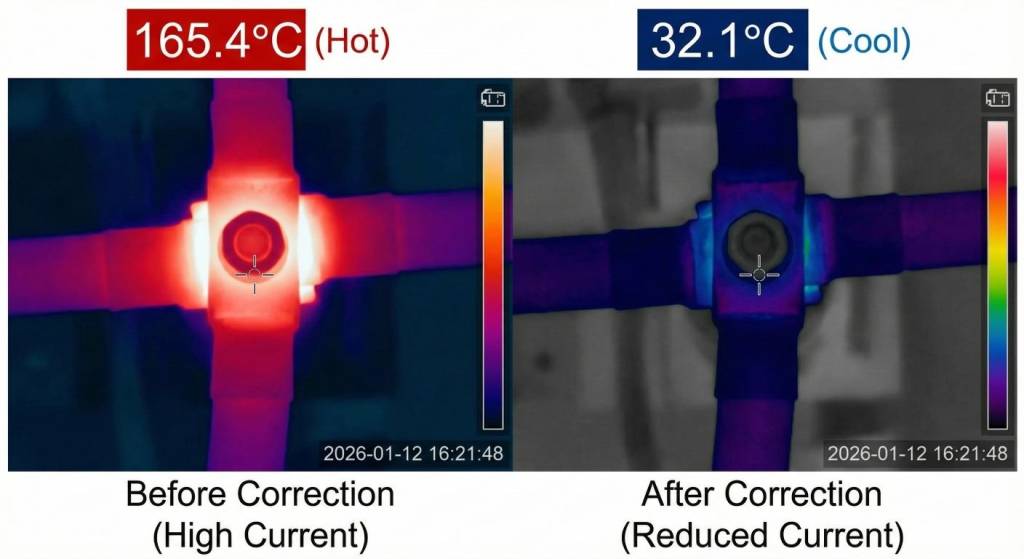

Compile a “Risk Improvement Dossier.” This should include the initial study report, installation certificates, before/after utility bills showing the efficiency gain, and thermographic scans showing the temperature reduction. Present this to your broker or the insurer’s risk engineer as part of your renewal submission.

Why This Resonates in the GCC: A Regional Context

In the GCC, operational cost reduction GCC strategies are vital due to specific regional drivers:

- Extreme Ambient Heat: Our electrical equipment already battles 50°C ambient temperatures. Adding internal heat from poor PF pushes equipment to its breaking point.

- High-Value Assets: The region is home to capital-intensive industries (Oil & Gas, Petrochemicals, Heavy Manufacturing). Insurers are keenly focused on asset protection here.

- Corporate Sustainability: Improving electrical efficiency aligns directly with ESG reporting, which is increasingly valued by global insurers and stakeholders.

Frequently Asked Questions (FAQs)

Q1: Is a guaranteed insurance discount provided for power factor correction?

No, it is not a guaranteed flat discount. Insurance underwriting is complex. However, it is a powerful demonstration of proactive risk mitigation that can positively influence your risk rating. This leverage can lead to better terms or help avoid premium increases. The direct utility savings provide the guaranteed, rapid financial ROI.

Q2: Our facility has variable loads. Is correction still effective?

Yes, but it requires a sophisticated approach. A proper study will determine if you need automatic capacitor banks that switch steps in and out in real-time to match the load. Fixed capacitors on variable loads can lead to over-correction, which is also dangerous.

Q3: Can poor power factor damage equipment that isn’t directly related to my utility bill?

Absolutely. The reactive current flows through all your distribution equipment—main transformers, switchgear, and long cable runs. This means you are paying for accelerated wear and tear on your entire electrical infrastructure, increasing long-term capital replacement costs.

Q4: We did a correction years ago. Do we need a new study?

Likely, yes. Electrical loads change over time with the addition of new machinery, LED lighting, and VFDs. An old correction system may now be under-sized or detuned, rendering it ineffective. A new study validates current performance and safety.

Conclusion

A Power Factor Correction study is a unique tool that turns a technical electrical efficiency project into a broader enterprise risk and financial management initiative. By reducing thermal stress on your system, you protect your assets, lower your bills, and build a compelling case for your insurer.

Don’t view your electrical system in isolation. Let us conduct a comprehensive Power Factor and Power Quality Study to quantify your direct savings, harden your infrastructure against failure, and build the evidence-based case for a stronger risk profile.

Contact our power systems specialists to schedule an assessment, or explore our Insurance & Risk Management services for a broader consultation.