Across the sun-drenched expanse of the Gulf Cooperation Council (GCC), the renewable energy revolution is fully underway. From the Mohammed bin Rashid Al Maktoum Solar Park in Dubai to the Sakaka IPP in Saudi Arabia, the region is home to some of the world’s largest and most cost-competitive solar projects. Yet, below the headline-grabbing gigaprojects lies a “missing middle.” Dozens of promising 50MW to 200MW commercial and industrial (C&I) or utility-scale projects stall every year, creating an estimated $500M financing gap.

The problem is rarely the financial model itself. The Internal Rate of Return (IRR) looks attractive, and the off-taker is often creditworthy. The bottleneck is Technical Bankability.

In the risk-averse environment of project finance, lenders, whether local giants like First Abu Dhabi Bank (FAB) or Saudi National Bank (SNB), or international development banks, do not just evaluate financial metrics. They scrutinize the engineering reality. If the technical assumptions underpinning the financial model cannot be vigorously defended with certified data, the project is deemed “unbankable.”

For developers, bridging this gap requires moving beyond basic feasibility studies to producing a comprehensive suite of technical evidence. This guide outlines the 7 critical documentation packages that form the bedrock of technical bankability renewable projects in the GCC.

The GCC Renewable Finance Landscape: Local vs. International Lender Expectations

Financing a renewable project in the Gulf involves navigating a unique ecosystem that blends international standards with regional specificities.

The Rise of Local Liquidity

Historically, international lenders drove the strict due diligence standards (like the Equator Principles). Today, local GCC banks have developed sophisticated project finance teams to support national visions (Saudi Vision 2030, UAE Net Zero 2050).

- Local Banks (GCC): Often prioritize the strength of the off-take agreement (PPA) and the EPC contractor’s local track record. They are increasingly requiring compliance with local content regulations (IKTVA/ICV).

- International Banks: Focus heavily on Environmental and Social Governance (ESG) compliance and strict adherence to IFC Performance Standards.

Islamic Finance Considerations

A significant portion of GCC renewable finance is structured as Islamic Finance (e.g., Istisna’a for construction, Ijara for operations).

- Asset-Backed Requirement: Unlike conventional loans which can be based on cash flow projections alone, Islamic finance requires tangible asset backing. The technical documentation must clearly define the physical assets (panels, inverters, land) to structure the Sharia-compliant contracts effectively.

- Sovereign Guarantees: In markets like Saudi Arabia, the Ministry of Finance often provides credit support for projects under the National Renewable Energy Program (NREP), but accessing this requires meeting rigid technical thresholds set by the energy ministry.

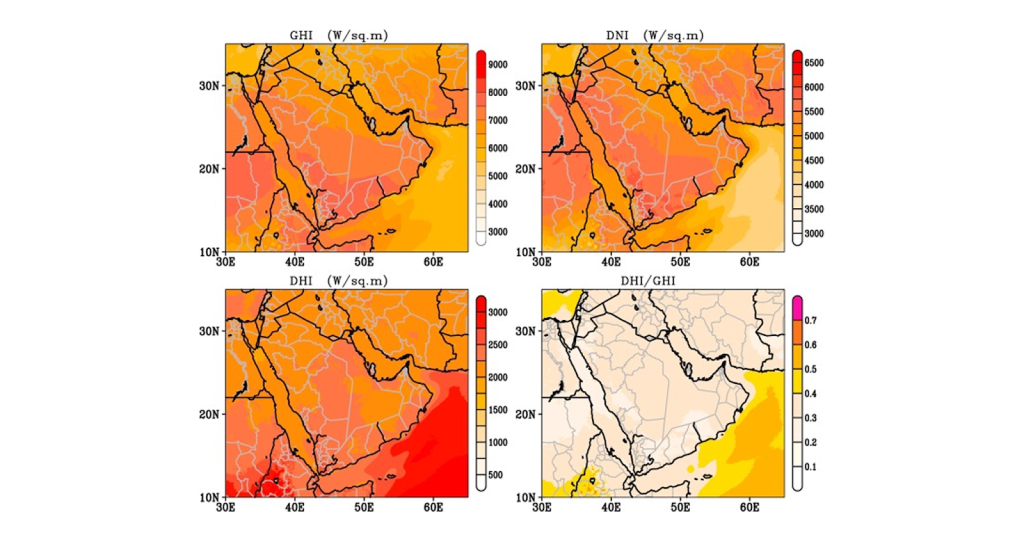

Documentation Package 1: Resource Assessment and Energy Yield Report

The sun may shine every day in the Gulf, but lenders do not fund “sunshine”; they fund “Probability of Exceedance.”

The Data Hierarchy

Lenders will reject yield predictions based solely on satellite data (like Solargis or Meteonorm).

- The Requirement: A minimum of 12 (ideally 24) months of on-site, ground-measured data using calibrated pyranometers. This ground data is used to correct the long-term satellite data, reducing uncertainty.

P50 vs. P90

The financial model usually runs on P50 (the yield expected 50% of the time). However, debt sizing is typically based on P90 or P99 (the yield exceeded in 90% or 99% of years).

- GCC Specifics: The energy yield analysis must specifically account for “Soiling Losses.” In the GCC, dust accumulation can reduce output by 0.5% to 1% per day if not cleaned. A report that assumes standard European soiling losses (2% per year) will be flagged as technically flawed by the Lender’s Technical Advisor (LTA).

[Placement for Image 1]

Documentation Package 2: Technology Due Diligence and Equipment Certification

Lenders are essentially buying the equipment for you. They need assurance that the technology will last for the 25-year tenure of the loan.

Tier 1 is Not Enough

Simply specifying “Tier 1 Solar Panels” is no longer sufficient.

- Bankability Reports: Lenders require specific bankability reports (like PV ModuleTech ratings) for the exact module model being used.

- GCC Certification: Equipment must have IEC 61215/61730 certification, but crucially, it must also meet local standards. For example, in Saudi Arabia, modules must be SASO certified. In UAE, inverters must be on the DEWA or ADDC approved list.

Degradation Warranties

The financial model assumes the plant degrades by ~0.5% per year.

- The Gap: Lenders scrutinize the warranty backing this. Is the manufacturer financially stable enough to honor a warranty claim in Year 15? Technology due diligence often requires a “Warranty Bond” or insurance wrap to protect the lender if the manufacturer goes bankrupt.

Documentation Package 3: Grid Integration Study and Connection Agreement

A solar plant that cannot export power is a stranded asset. The grid integration study is the proof of connectivity.

The Holy Trinity of Studies

Lenders require three distinct electric power system analysis studies, approved by the utility (SEC/DEWA/Transco):

- Load Flow: Proving the grid can accept the power without thermal overload.

- Short Circuit: Ensuring the plant doesn’t exceed the grid’s fault level rating.

- Dynamic Stability: Crucial for renewables. Proving the plant stays connected during grid faults (Fault Ride Through).

Firm vs. Non-Firm Connection

The utility connection agreement dictates revenue.

- Firm Access: The utility guarantees it will take your power.

- Non-Firm (Curtailable): The utility can order you to stop generating during grid congestion. Lenders hate this risk. If the connection is non-firm, the technical advisor must model the expected curtailment losses (e.g., 3%) to adjust the revenue forecasts.

Documentation Package 4: EPC Contractor Qualification and Track Record

The Engineering, Procurement, and Construction (EPC) contract is the primary vehicle for delivering the project. Lenders assess the Electrical Plant Procurement strategy to ensure the “Jockey” (Contractor) is as capable as the “Horse” (Project).

Financial Strength

The EPC contractor must have a balance sheet strong enough to support the Performance Bonds (typically 10-20% of contract value). Small, local contractors often fail this test unless backed by a larger parent company.

Relevant Experience

“Solar experience” is too vague. Lenders look for EPC contractor qualification specific to:

- Technology: Have they built projects with the specific tracking system or central inverters proposed?

- Geography: Have they built in the GCC desert? A contractor experienced in Germany may underestimate the cost of civil works in rocky desert terrain or the logistics of water supply for cleaning.

Documentation Package 5: Operations and Maintenance (O&M) Strategy

Once built, the plant must perform. The O&M contract is the lender’s assurance of long-term asset health.

The Scope of Service

Lenders require a detailed O&M strategy renewable plan that covers:

- Preventive Maintenance: Scheduled checks.

- Corrective Maintenance: Response time guarantees (e.g., “Site attendance within 4 hours”).

- Spare Parts Management: A bonded warehouse with critical spares (inverters, motors) located within the country to minimize downtime.

Cleaning Strategy

In the GCC, cleaning is the single most critical O&M activity. The documentation must specify:

- Method: Robots (water-free) vs. Tractor/Truck (water-based).

- Frequency: Defined cycles (e.g., twice a week for robots, twice a month for wet cleaning).

- Performance Guarantee: The O&M contractor must guarantee a minimum Performance Ratio (PR) or Availability, backed by Liquidated Damages (LDs).

Documentation Package 6: Environmental and Social Impact Assessments (ESIA)

Even for clean energy, environmental impact assessment is mandatory and rigorously checked by lenders adhering to the Equator Principles.

Water Usage

In a water-scarce region, a solar plant consuming millions of liters of water for cleaning is a major environmental risk.

- The requirement: Lenders prefer robotic dry-cleaning solutions to minimize the Water Footprint. If wet cleaning is used, the source (desalinated vs. groundwater) and disposal method must be permitted.

Social License

For projects in remote areas, ESG compliance GCC requires a “Local Content Plan.” How will the project benefit the local Bedouin or rural communities? Employment quotas and training programs are often written into the loan covenants.

Documentation Package 7: Decommissioning and End-of-Life Plan

Lenders hold the risk until the end. They need to know what happens in Year 25.

The Decommissioning Plan

A technical report detailing:

- How the panels and steel will be dismantled.

- How the land will be restored to its original state.

- Recycling: A strategy for recycling PV modules (a growing regulatory requirement in UAE and KSA).

The Decommissioning Bond

Lenders often require the project company to build up a decommissioning reserve fund starting from Year 10 or 15, ensuring cash is available to pay for removal even if the project company becomes insolvent at the end of the PPA.

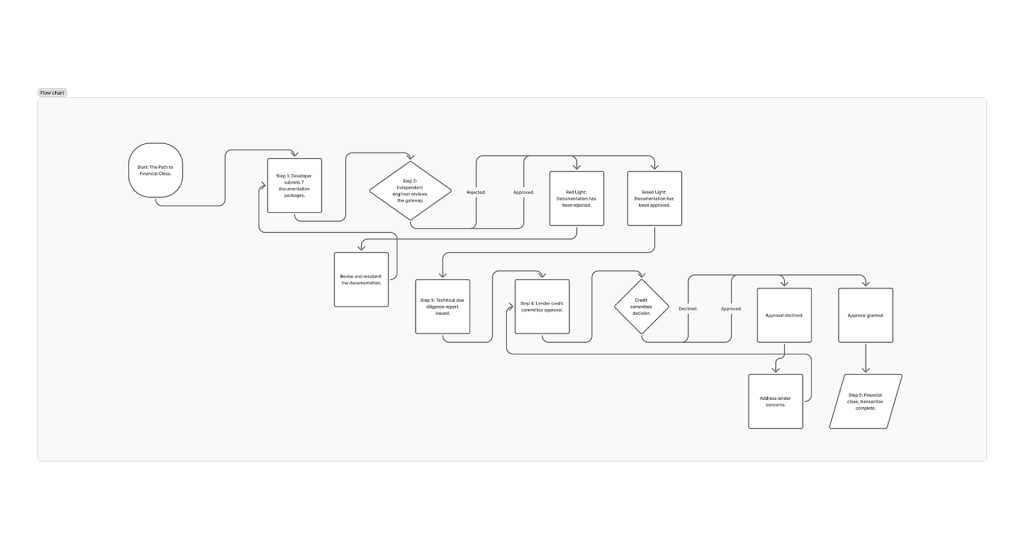

The Independent Engineer’s Role: Validating Technical Assumptions for Lenders

Lenders do not trust the developer’s data implicitly. They hire an Independent Engineer (IE) or Lender’s Technical Advisor (LTA) to audit everything.

The IE produces the “Bankability Report,” a 100+ page document that validates:

- “The P90 yield is realistic.”

- “The EPC contract price is within market norms.”

- “The technology is proven.”

Without a clean report from a reputable IE, the credit committee will not approve the loan.

Frequently Asked Questions (FAQ)

1. What is the difference between P50 and P90 energy yields?

P50 is the best estimate; there is a 50% chance the actual generation will be higher or lower. P90 is a conservative estimate; there is a 90% chance the generation will exceed this figure. Lenders use P90 (lower revenue) to stress-test the Debt Service Coverage Ratio (DSCR).

2. Can we use new, cutting-edge solar panels for a financed project?

It is difficult. Lenders prefer “proven” technology with a track record of at least 2-3 years in the field. Using unproven tech often requires a “Technology Wrap” insurance policy or higher equity contribution from the developer.

3. Why do GCC lenders care about the cleaning method?

Because soiling losses in the GCC can reach 50% in a month without cleaning. If the cleaning strategy fails, the revenue collapses, and the loan defaults. Lenders view the cleaning robot warranty and maintenance contract as a critical security document.

4. Is the grid connection study required before financial close?

Yes. Lenders will not take “grid risk.” They need a signed Interconnection Agreement or a firm offer from the utility confirming that the grid has the capacity to evacuate the power the plant generates.

5. Do Islamic banks have different technical requirements?

The technical standards (yield, safety, quality) are the same. However, the structure of the contracts differs. The technical specs must be extremely precise because, in Islamic finance (like Istisna’a), the bank is technically “buying” the asset to lease it back to you. Ambiguity in specs creates Sharia compliance issues.

Conclusion: Engineering the Finance

In the modern era of GCC infrastructure, finance and engineering are inextricably linked. A renewable energy project is not merely a construction effort; it is a financial product structured around technical performance. The “Bankability” of a project depends as much on the robustness of its yield curves and the durability of its inverters as it does on the credit rating of its off-taker.

For developers and project sponsors, the lesson is clear: Do not treat technical documentation as a box-ticking exercise for the end of the development cycle. It is the foundation of your financing strategy.

Secure your project’s financial future.

Bridging the gap between technical reality and lender expectations requires a specialized partner. Elecwatts serves as a trusted net zero electrical engineering consultancy to developers and lenders across the region. We prepare bankable yield assessments, conduct rigorous technology due diligence, and manage grid integration studies that stand up to the scrutiny of the toughest credit committees.

Contact Elecwatts today to ensure your renewable project is built to be bankable.